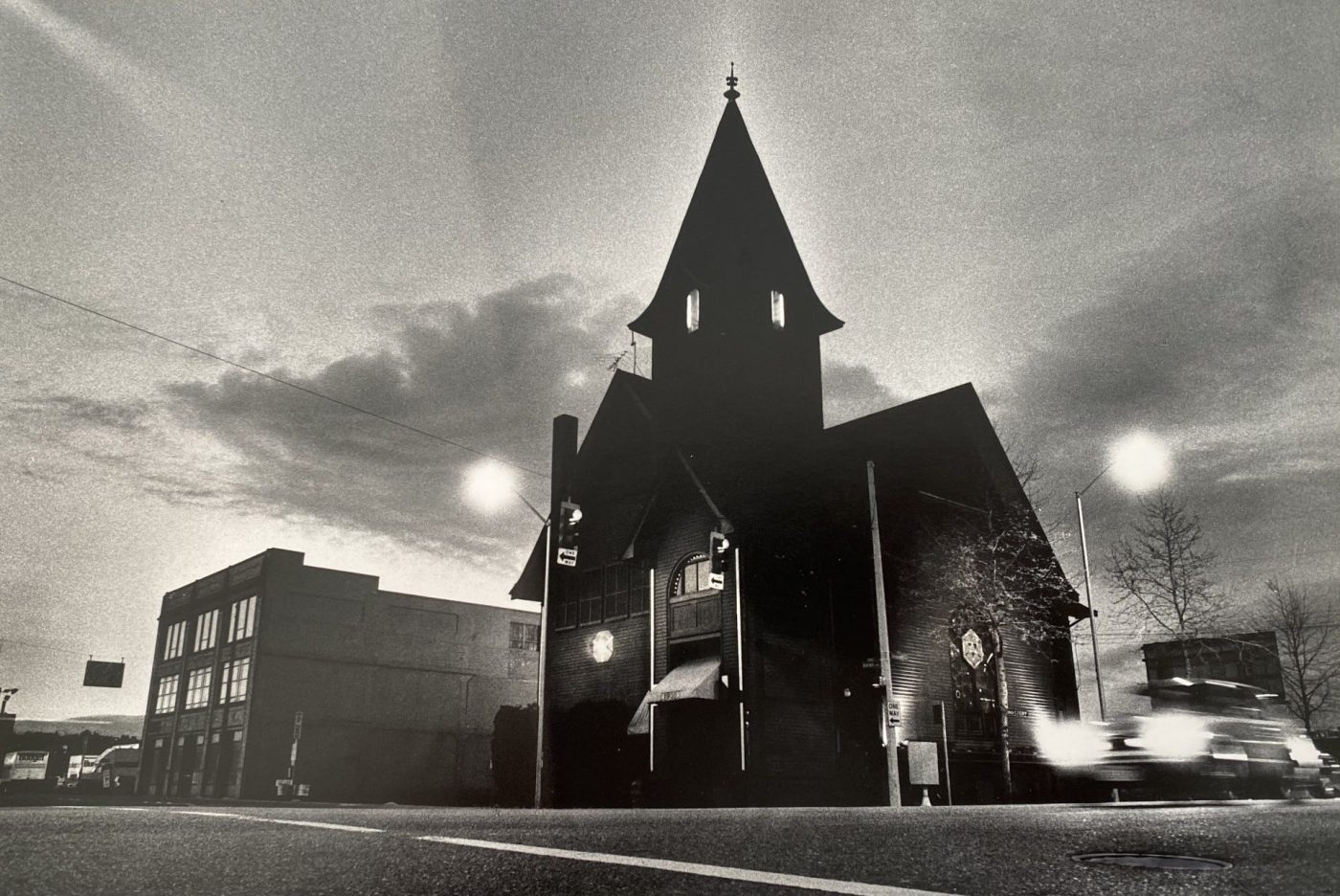

The Monastery

In 1977, George Freeman, a New Yorker, moved to Seattle and found a derelict church with a “For Rent” sale on it. George – an opportunist – formed The Monastery Church, and focused his attention on turning it into a night establishment. On May 19, 1979, George Freeman became the Presiding Minister for The Monastery, A Universal Life Church Congregation. Reverend Freeman was fundamental to the advancement of the church. Eventually, he used the space as a nightclub and refuge in the downtown neighborhood of Seattle.

On January 1st 1982, Reverend Freeman went to trial in front of The Board of Tax Appeals. He stood accused of owing a little over one thousand in back-taxes. Reverend Freeman challenged this and claimed that he was exempt from the fees. The church was a nonprofit organization, and a church, no less. Reverend Daniel Zimmerman, Freeman’s administrative assistant, claimed that all the funds from members of the congregation were given voluntarily. He claimed further that Reverend Freeman always acted properly in the collection and distribution of church funds. In addition, Reverend Freeman rightfully claimed the space was a shelter for the many homeless gay youth and adult population of Seattle. The space was a benefit to the community and the congregation. These claims were successful. The judge ruled that the property was tax exempt when the space was used for church purposes.

Despite the opposition by the police and other members of the local community, the judge decided that The Monastery was fundamental for Seattle’s disenfranchised youth and provided a necessary community service. The Board of Tax Appeals continued to dispute that The Monastery, Universal Life Church, Inc., was a church. However, the court decided that the dancing equipment and speakers were not part of typical church activity. As a result, they were then taxed.